")

Bruce Bennett/Getty Images News

2022 has been a wild ride for Kohl’s (NYSE:KSS) shareholders. After a failed sales process and massive earnings shortfall (discussed below), shares have been cut in half in 2022.

However, I believe that normalized earnings are nearly double the current levels. Further, the continued presence of activist shareholder Macellum, recent departure of several top executives, and significant real estate value (discussed below) suggest the company remains ‘in play’ for a buyout should financing conditions improve.

Current Conditions

Cost inflation and a weaker consumer spending environment have caused Kohl’s to significantly underperform its initial 2022 guidance. Entering 2022, Kohl’s had expected to earn $7-7.50 per share. After reducing guidance upon the release of 2Q results, Kohl’s scrapped the guidance all together when it reported 3Q results:

Guidance Withdrawn (Kohl’s 3Q22 Earnings Transcript from Seeking Alpha)

Beyond internal issues (departure of CEO, CMO) like most retailers Kohl’s has been suffering from a difficult retail environment. Factors which have depressed results include:

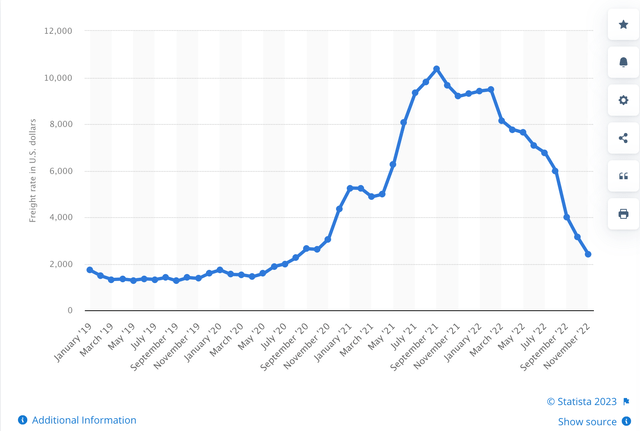

- Higher international freight expenses – while these have been a significant headwind throughout 2022, as shown below, freight costs have plummeted and should be a meaningful tailwind going forward

Global Container Freight Index (Statista)

- Inflationary pressure on COGS, wages, and utilities. Inflationary pressure on COGs has fallen as both global freight (shown above) but also cotton have fallen.

- Consumers have been pressured by inflation throughout 2022 which has led to a slowdown in spending on discretionary items like apparel.

- Retailers have too much inventory which has created a highly promotional environment.

As we sit today, consensus earnings estimates for Kohl’s are just $3.05 per share (-58% versus the midpoint of original 2022 and -59% versus 2021 actual EPS).

‘Normalized Earnings’ & Valuation

While the current results are depressing due to the factors cited above, I hope that the results will improve as:

- Retailers will work their way through the current inventory glut. While this involves a painful period of heavy discounting (which negatively impacts current gross margins), this will lead to a better matching of future supply and demand, leading to a rebound in gross and operating margins.

- International freight expenses are declining – this will further benefit gross margins.

- Consumer confidence and spending on discretionary purchases like apparel should improve as inflation subsidies.

Historically Kohl’s has generated operating margins in the 6-9% range over the past decade. I assume that Kohl’s can produce a 6.5% normalized operating margin on a base of $18 billion in revenue which gets me to an estimate of $5.80 in normalized EPS.

My 6.5% operating margin is at the low end of the historical range and takes into account the increased pressure the business has felt from off-price retailers such as TJX Companies (TJX), Ross Stores (ROST) and Burlington (BURL). In recent years we’ve seen that department stores like Dillard’s (DDS) and Macy’s (M) improve their fortunes through cutting costs and improving merchandising/brand partnerships. Kohl’s should be able to benefit from some of these types of initiatives as well. For example, I expect that the expansion of Kohl’s partnership with Sephora will lead to a rebound in foot traffic and sales.

Applying an 8-10 P/E multiple to my normalized EPS estimate yields a value of $45-58 per share implying 78-130% upside.

Real Estate Values

Given that Kohl’s has been evaluating a sale and that its real estate has been seen as a significant component of its value, I have attempted to value the company’s real estate holdings. While rising interest rates and a difficult transaction financing environment were partly to blame for the failure of a sales process, the financing environment should improve/decrease interest rates, I hope that we could see a deal of speculation picking up again.

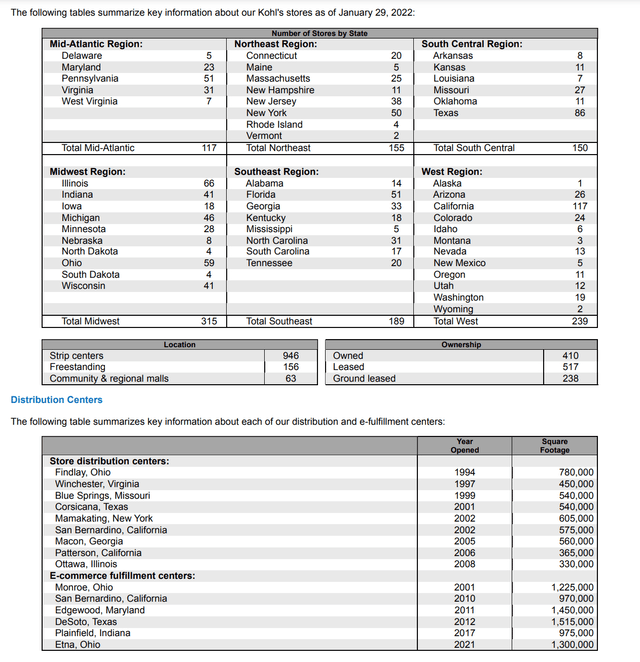

Kohl’s has accumulated a significant real estate portfolio -the company owns over 600 retail properties in shopping centers throughout the country as well as some warehouses.

Real Estate Holdings (Kohl’s 2021 10-K)

As shown above, Kohl’s owns the land and building for its 410 stores. Further, the company owns the building (but leases the land) for another 238 stores. Below I attempt to conservatively estimate the value of Kohl’s real estate holdings:

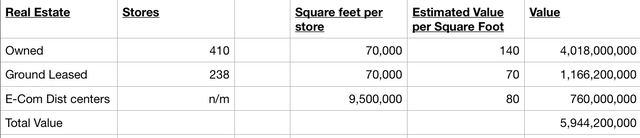

Kohl’s Real Estate Valuation (Company Filings; Author Estimates)

As shown above, I estimate that Kohl’s real estate is worth about $6 billion. To value its retail real estate portfolio, I assigned a value of $140 per square foot to the properties where Kohl’s owns both the land and building. These properties are predominantly located in shopping centers. This compares to an implied valuation of $175-255 per foot for shopping center REITs like Brixmor (BRX), Kimco (KIM), and Kite Realty (KRG).

I value Kohl’s fully owned retail real estate at a discount because the aforementioned shopping center REITs have made significant progress in whittling down their real estate holdings by divesting properties with inferior demographic characteristics over the years. Kohl’s has not gone through an equivalent divestiture process and likely owns many less desirable properties. In addition, a buyer for Kohl’s properties would likely incur expenditure to re-tenant any space Kohl’s looks to shed (in most cases involving a reconfiguration of the space as very few tenants require ~70k square feet of space).

I assume that properties where Kohl’s does not own the building have a valuation equal to half the fully owned properties. I then value the company’s owned warehouse real estate at $80 per square foot. This is at the low end of the comparable range for warehouse real estate ($100-250 per square foot).

Kohl’s has a total enterprise value (market cap plus net debt) of $7.5 billion. Based on my estimate, Kohl’s real estate accounts for 80% of its enterprise value. This implies that the company’s retail operation (deducting pro-forma additional rent expense that would be incurred in a separation of retail and real estate) trades at an implied value of just 2x normalized operating profit. Were the company able to unlock the real estate value in a tax efficient manner and the market to apply a 6x multiple to its pro-forma operating profit (after adjustment for higher rent paid), Kohl’s would be worth $65 per share.

Conclusion

Kohl’s is a challenging business operating in a competitive environment. That said, I don’t believe that current results are reflective of the medium term earnings power of the business. Assuming a modest improvement in the external environment, Kohl’s shares look to have a significant upside. As such, I’ve taken a small position in the stock.

+ There are no comments

Add yours